The Vital Role of Food Manufacturing Insurance

In the dynamic and ever-evolving landscape of the food manufacturing industry, success hinges on a combination of quality products, efficient processes, and meticulous risk management. Amidst the myriad challenges faced by food manufacturers, one often underestimated cornerstone of risk management is food manufacturing insurance. In an industry prone to a range of perils, from supply chain disruptions to product recalls, having comprehensive insurance coverage specifically tailored for food manufacturing is not just a precautionary measure, but an essential strategic asset. This article delves into the pivotal importance of food manufacturing insurance, emphasizing key coverage types including public liability, employers liability, and material damage, and the considerations that can shield businesses and foster enduring success.

The Unique Risks of Food Manufacturing

Food manufacturing is a complex and high-stakes industry, laden with distinctive risks that necessitate specialized insurance solutions. These inherent risks encompass:

- Product Liability: The potential for contaminated or substandard food products, and the subsequent health risks to consumers, poses a considerable liability. This underlines the critical role of robust product liability coverage.

- Supply Chain Disruptions: Food manufacturers are vulnerable to supply chain disruptions caused by factors like natural disasters, transportation delays, and regulatory changes. Such disruptions can lead to production halts, revenue loss, and diminished customer trust.

- Property Damage: The extensive physical assets involved in food manufacturing, including processing equipment and inventory, are susceptible to damage from fires, equipment failures, and unforeseen accidents.

- Product Recalls: Contaminated or mislabeled products can necessitate costly and reputation-damaging recalls. Adequate product recall insurance becomes instrumental in managing the financial and reputational fallout.

- Business Interruption: Unpredictable events such as fires or equipment breakdowns can disrupt operations, resulting in significant revenue loss. Business interruption insurance provides a crucial safety net during such disruptions.

Key Types of Food Manufacturing Insurance

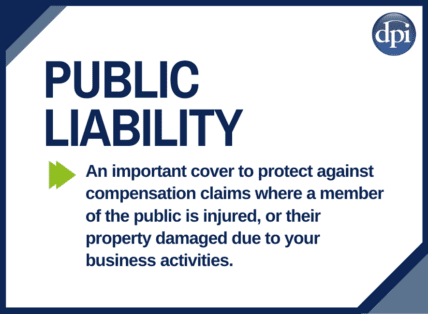

- Public Liability Insurance for Food Manufacturers: This indispensable coverage safeguards against claims of third-party bodily injury or property damage occurring within your premises or due to your products. Given the manufacturing environment’s inherent risks, public liability insurance tailored for food manufacturing is non-negotiable.

- Employers Liability Insurance: In the event of work-related employee injuries or illnesses, employers liability insurance provides financial protection against potential legal and medical expenses, ensuring the well-being of your workforce and the longevity of your business.

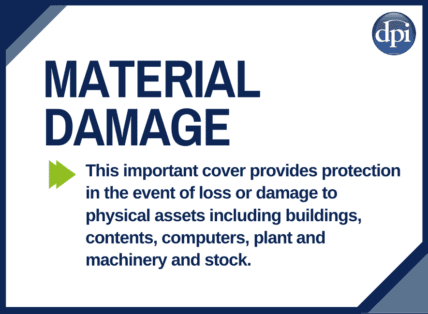

- Material Damage Insurance: This form of insurance covers the gamut of physical assets, encompassing buildings, equipment, and inventory. For food manufacturers, where operational machinery is paramount, material damage insurance takes center stage.

- Business Interruption Insurance: Unexpected disruptions can wreak havoc on a food manufacturer’s bottom line. Business interruption insurance alleviates the financial strain during operational downtime.

- Supply Chain Disruption Insurance: The food supply chain is vulnerable to a plethora of disruptions. Tailored insurance solutions can help mitigate the financial ramifications of such supply chain interruptions.

- Product Recall Insurance: In the unfortunate event of a product recall, this specialized insurance alleviates the financial burden of consumer notifications, product retrieval, and overall recall management.

- Cyber Insurance: With digitalization sweeping the industry, cyber insurance becomes paramount to mitigate the escalating risks of data breaches and cyber incidents.

Considerations for Choosing Food Manufacturing Insurance

- Risk Assessment: Thoroughly assess the unique risks inherent in food manufacturing to ascertain the optimal types and levels of insurance coverage required.

- Adequate Coverage Limits: Ensuring that coverage limits align with potential losses is crucial, considering the scale and complexity of food manufacturing operations.

- Exclusion Evaluation: Scrutinize policy exclusions meticulously to understand which risks are excluded from coverage, enabling alternative risk management strategies.

- Optimal Deductibles: Balancing deductibles with premium costs is pivotal, as higher deductibles can lead to cost savings but require greater out-of-pocket expenses during claims.

- Reputable Insurer Selection: Collaborating with reputable insurance companies renowned for efficient claims handling and robust client support is a prudent approach.

Conclusion

Navigating the intricate realm of food manufacturing demands not only unwavering commitment to quality but also a comprehensive strategy to mitigate risks. Food manufacturing insurance, tailored to the sector’s distinct challenges, stands as an irreplaceable cornerstone of this strategy. By grasping the inherent risks, selecting apt coverage, and partnering with esteemed insurers, food manufacturers can confidently confront challenges, safeguard their assets, and secure the enduring prosperity of their endeavors in a relentlessly competitive market.